Does Market Timing Work?

Interesting results for such a frequent question!

Happy April to all my dozens of readers out there!

This month, our newsletter is going back to basics. After a great Q1 in 2024 for the US markets, inflation coming up to 3.5% in America and interest rates being held still in the 5.25% to 5.5% range, it is as important as always to step back from all the short-termism and day-today volatility and focus. Focus on what works and focus on your long-term strategy.

I had got a penny for each time a client asked me about market timing, I wouldn't be writing this right now - or maybe I would, but from a bungalow in the Caribbean. I would like to share a summary of a great article I found on Charles Schwab Financial Research - and I am sure most of you will appreciate the richness of the information.

And, before you forget:

1- Do you want to skip the whole article?

So, here is the main finding: There's a high cost to waiting for the best entry point.

2- I have a lump of cash: what do I do now?

Imagine for a moment that you've just received a year-end bonus . You're not sure whether to invest now or wait. After all, the market recently hit an all-time high. Now imagine that you face this kind of decision every year—sometimes in up markets, other times in downturns. Is there a good rule of thumb to follow?

(Funny enough, many of my clients have just received their annual bonuses and the US markets have just reached their all-time highs - that's why I saw this article so timely and interesting!).

Schwab Research found that the cost of waiting for the perfect moment to invest typically exceeds the benefit of even perfect timing. And because timing the market perfectly is nearly impossible, the best strategy for most of us is not to try to market-time at all. Instead, make a plan and invest as soon as possible.

3- Five different styles

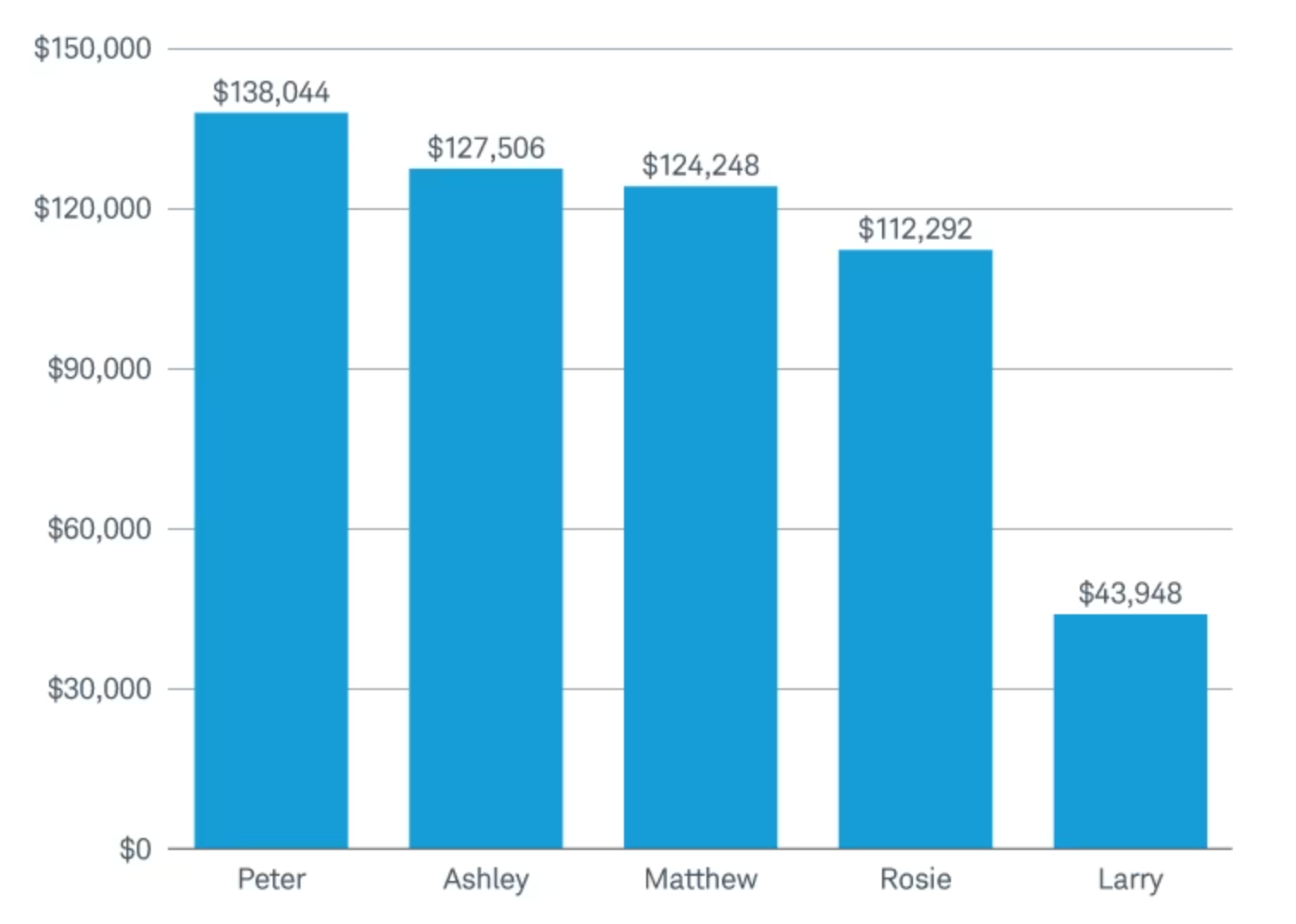

Let's assume 5 different investors received $2,000 at the beginning of every year for the 20 years ending in 2022 and left the money in the stock market, as represented by the S&P 500® Index (although diversification and the use of different asset classes may be fundamental when building your portfolio, they only considered US equities to easily measure the results of market timing). Here are the results:

Peter Perfect was a perfect market timer. He had incredible skill (or luck) and was able to place his $2,000 into the market every year at the lowest closing point. For example, Peter had $2,000 to invest at the start of 2003. Rather than putting it immediately into the market, he waited and invested on March 11, 2003—that year's lowest closing level for the S&P 500. He continued to time his investments perfectly every year through 2022.

Ashley Action took a simple, consistent approach: Each year, once she received her cash, she invested her $2,000 in the market on the first trading day of the year.

Matthew Monthly divided his annual $2,000 allotment into 12 equal portions, which he invested at the beginning of each month. This strategy is known as dollar-cost averaging.

Rosie Rotten had incredibly poor timing—or perhaps terribly bad luck: She invested her $2,000 each year at the market's peak. (the opposite of Peter Perfect!)

Larry Linger left his money in cash investments (using Treasury bills as a proxy) every year and never got around to investing in stocks at all. He was always convinced that lower stock prices—and, therefore, better opportunities to invest his money—were just around the corner.

4- The Results

For the winner, look at the graph, which shows how much hypothetical wealth each of the five investors had accumulated at the end of the 20 years (2003-2022). Actually, Schwab has looked at 78 separate 20-year periods in all, finding similar results across almost all time periods.

Of course Peter won - but it is quite amazing to see that Ashley was less than 8% behind Peter! Especially considering that Ashley had simply put her money to work as soon as she received it each year—without any pretense of market timing.

But, for me, the most astonishing and important takeaway is: even BAD MARKET TIMING TRUMPS INERTIA. And Rosie crushed Larry's results - and she was only $15,000 behind Ashley and got 3 times more money than Larry after 20 years.

5- What about other time-periods?

Schwab analyzed all 78 rolling 20-year periods dating back to 1926 (e.g., 1926-1945, 1927-1946, etc.). In 68 of the 78 periods, the rankings were exactly the same: Peter Perfect was first, Ashley Action second, Matthew Monthly third, Rosie Rotten fourth, and Larry Linger last.

But what about the 10 periods when the results were not as expected? Even in these periods, investing immediately never came in last. It was in its normal second place four times, third place five times and fourth place only once, from 1962 to 1981, one of the few extended periods of persistently weak equity markets. What's more, during that period, fourth, third and second places were virtually tied.

6- Schwab's Conclusion

Realistically, the best action that a long-term investor can take, based on our study, is to determine how much exposure to the stock market is appropriate for their goals and risk tolerance and then consider investing as soon as possible, regardless of the current level of the stock market.

6.1 - Adddendum

Consider dollar-cost averaging as a compromise

If you don't have the opportunity, or stomach, to invest your lump sum all at once, consider investing smaller amounts more frequently. As long as you stick with it, dollar-cost averaging can offer several potential benefits:

Prevents procrastination. Some of us just have a hard time getting started. We know we should be investing, but we never quite get around to it. Dollar-cost averaging helps you invest consistently.

Avoids market timing. Dollar-cost averaging ensures that you will participate in the stock market regardless of current conditions. While this will not guarantee a profit or protect against a loss in a declining market, it will eliminate the temptation to try market-timing strategies that rarely succeed.

7- My conclusion (and advice…)

There are two things everyone should think about (and make a contract with oneself!) if they want to be successful in their investing journey:

Extend your time-horizon: if you commit to anything less than 5 years in the stock market (some may say 7, 8 or 10!) your chances of making money and doing well with your investments are dramatically reduced.

Have your emergency funds in place: BY A MILE, one of the most important things that make an investor resilient to volatility, market crashes or unexpected life misfortunes is a LIQUID and PROTECTED emergency fund. I have been working long enough in this industry to see people going “all in" just to see themselves with no option but to sell at a big loss because they needed some money.

Once you have these 2 in place, build a diversified, sturdy, low-cost portfolio and chose whatever you feel more comfortable with: lump sum or regular investments.

Actually, there is also a 3rd option: you can invest in thirds! Send 33% in and commit to send the other 2 thirds in 1 and 2 months from that time (or 2 and 4, why not?). Benefits of investing in thirds: a chunk is invested right away, if the market goes up, you already got some at a lower cost-basis; if the market goes dow, you have the opportunity to buy more at a cheaper price! Either way, YOU WIN!

;-)

Disclaimer: as always, this newsletter should never be considered as personal financial advice. Always consult an specialist or take full responsibility for your choices and strategies.

Do you want to hear more about a specific subject? Send me a message or leave a comment at the bottom! All ideas are welcome!

Wanna read the full article? Just click below:

And do not forget to share the love!

One of the four most exciting time of the year (for me) is just starting! Q1 earning season has just begun! So, a lot to talk about next month…

Have an amazing Sunday ahead and see you in May!